Medicare is Complicated. We Make It Simple.

At first glance, the Medicare process can seem overwhelming. Our team at Carolina Insurance Professionals can help make the process simple and easy to understand.

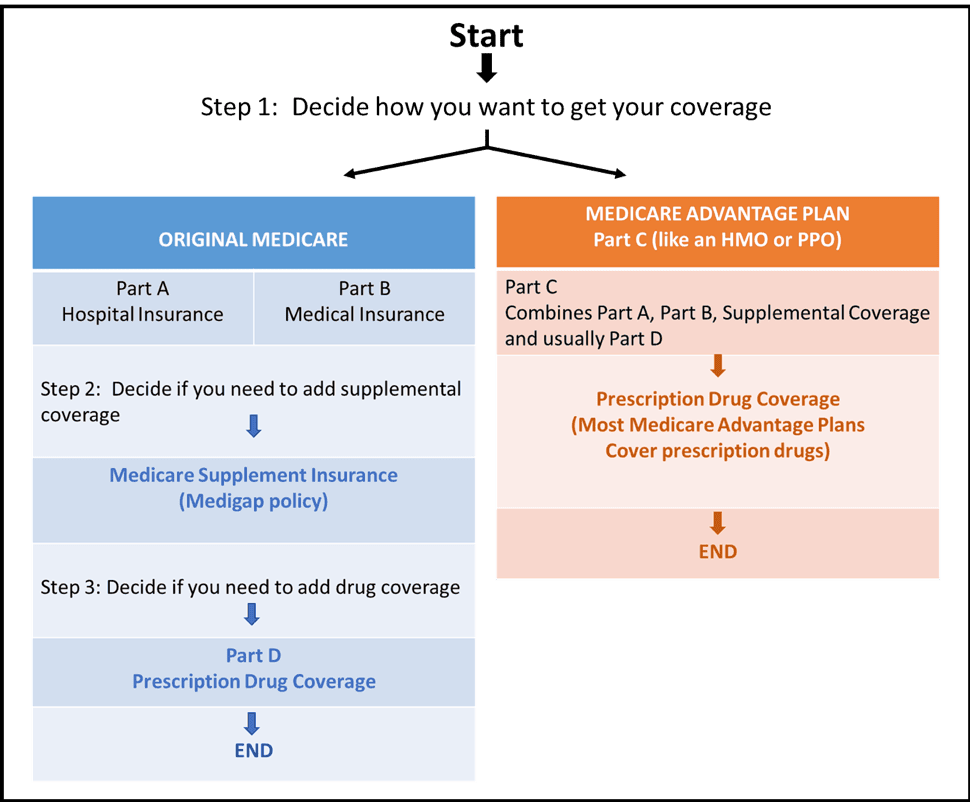

Here are the Medicare Basics:

Give us a call today and we can get started on walking you through this process.

Find The Perfect Plan

Fill out the form below, and one of our agents will be in touch as soon as possible.

"*" indicates required fields

Want To Speak with an Insurance Agent?

Call Us at 919-285-4732

How Our Clients Rate Us

“I HIGHLY recommend Carolina Insurance Professionals! I have been using them for 4 yrs and they are the BEST! Ronee takes the highly complex world of insurance (esp health insurance) and makes it easier to understand. Without her assistance I would not have been able to navigate the selection of med insurance policies the last four years.”

Susan Stephens

“This company has integrity and professionalism written all over it. I have had Jayson Green (sp?) helping me for the past couple years and he's saved me over $1000 on my premiums and prescription prices. If you're on the fence about giving them a call, do it.”

Max Foley

“Ronee and Jayson have been so helpful, patient and informative. Health insurance is confusing. Medicare is even more confusing. They helped sort it all out for us, got us set up and we feel very confident we have the right policies, the right pricing and best information. Thanks so much👍”

Dona Lerner